Nearly $31 billion in utility rate increases were requested by U.S. electric and gas utilities in 2025, more than double the prior year, with projected effects on 81 million Americans according to PowerLines' year-end review. That figure changes the frame. The energy cost increase isn't just a story about commodity volatility or weather. It's a story about how geopolitical shocks, fuel markets, grid constraints, regulatory choices, and new sources of demand converge inside household bills.

That convergence matters because voters don't pay “global risk.” They pay a monthly bill shaped by local tariffs, utility capital plans, fuel adjustment mechanisms, and state regulatory decisions. A maritime security crisis can tighten fuel markets abroad, but the political consequences surface domestically when commissions approve rate recovery and households absorb the cost. Recent disruptions in strategic waterways, including the Red Sea attacks and shipping risk escalation, illustrate how quickly distant instability can enter domestic inflation politics.

Table of Contents

- The Unfolding Energy Price Crisis

- Deconstructing the Price Spike Short and Long-Term Drivers

- From Global Markets to Household Wallets

- How Grid Infrastructure and New Demand Add to Costs

- Analyzing the Economic and Political Fallout

- Navigating the New Energy Reality Policy Levers and Takeaways

The Unfolding Energy Price Crisis

U.S. households and firms are paying more for energy even when the grid remains operational and fuel is available. That pattern points to a system-wide pricing problem, not a simple shortage story.

The current energy cost increase works through several layers at once. Geopolitical shocks raise the cost of fuel and shipping. Utilities then file to recover higher purchased power, storm hardening, wildfire mitigation, and financing costs through regulated rates. State commissions decide how those costs are allocated across residential, commercial, and industrial customers. The result is a delayed but durable pass-through from global disruption to monthly bills.

Recent maritime insecurity shows the mechanism clearly. Disruptions to shipping lanes, including the Houthi attacks in the Red Sea, have raised transport risk, insurance costs, and delivery times across energy and commodity supply chains. Even where the direct fuel effect is limited, those disruptions tighten equipment markets, complicate procurement, and raise the cost of grid expansion and maintenance.

A crisis of transmission, not just supply

The pressure now sits inside the regulated system. Higher energy bills often reflect more expensive inputs, more expensive capital, and broader cost recovery requirements rather than blackouts or physical scarcity. That distinction has political consequences. Voters experience the increase as a utility failure, while many of the drivers originate in foreign policy shocks, supply-chain friction, and domestic regulatory choices.

A practical rule follows. Once energy affordability becomes a recurring rate-case issue, it becomes a governance problem as much as a market problem.

Three channels deserve attention:

- Global fuel exposure: Domestic power prices still absorb international shocks because natural gas, fuel transport, and equipment supply chains remain globally linked.

- Infrastructure cost recovery: Transmission upgrades, resilience projects, and deferred maintenance are increasingly folded into retail rates.

- Load concentration: New data center demand can trigger local substation, transmission, and generation investments. Whether those costs stay with the new load or spread to the wider rate base depends on utility tariff design and commission decisions.

For policymakers, the implication is clear. Energy affordability now sits at the intersection of sanctions policy, utility regulation, and industrial development. A government can respond to a geopolitical crisis abroad and still worsen household energy pressure at home if rate design, interconnection policy, and large-load cost allocation are handled as separate questions.

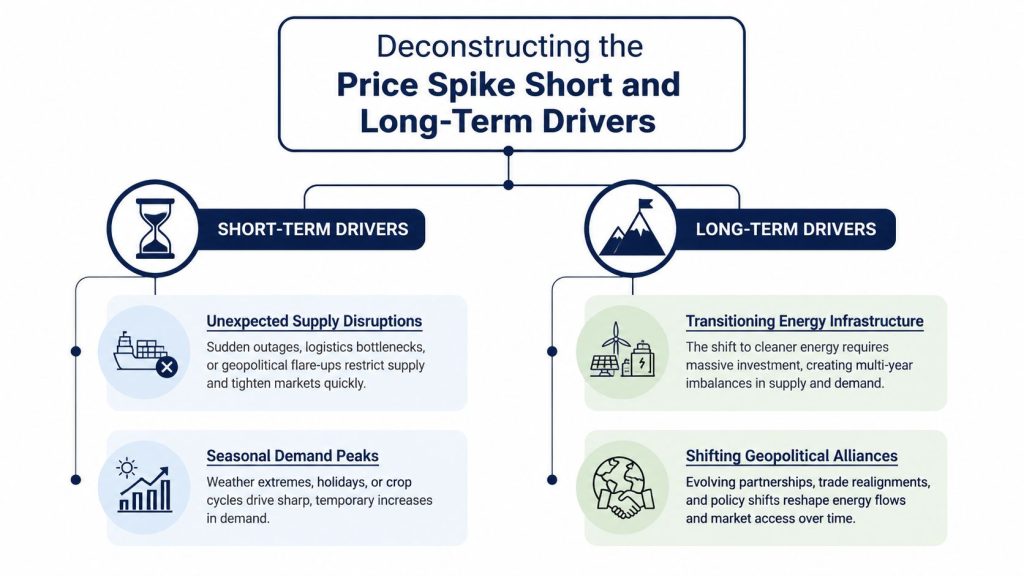

Deconstructing the Price Spike Short and Long-Term Drivers

The immediate temptation is to blame any energy cost increase on one event. A war. A sanctions package. A cold winter. A heat wave. That lens is too narrow. Short-term shocks determine where prices jump first. Long-term pressures determine how long the jump lasts and how broadly it spreads.

A useful market frame appears in this broader energy market analysis. Energy systems are now exposed to both event risk and structural fragility. That combination is why price relief often proves slower than political leaders expect.

Short-term shocks change fuel costs first

The clearest recent example comes from U.S. power markets. The U.S. Energy Information Administration reported that Benchmark Henry Hub spot gas prices averaged $3.52 per million British thermal units in 2025, 56% higher than in 2024, and that average wholesale day-ahead electricity prices at most major trading hubs in the Lower 48 were higher in 2025 than in 2024, largely because of higher natural gas prices to generators, according to the EIA's review of wholesale electricity prices and generation trends.

That matters for two reasons.

First, it shows why geopolitics reaches retail power markets even without a physical shortage at home. Sanctions, shipping insecurity, and regional conflict can tighten global gas balances or raise risk premiums. In gas-linked systems, the marginal price of power follows.

Second, the EIA data show that total electricity generation in the Lower 48 increased 2% in 2025, yet natural gas-fired generation fell 3%, offset by an 11% rise in coal generation and a 32% rise in solar generation. The lesson is analytical. Higher prices don't necessarily mean the system produced less electricity. They can mean the system produced electricity from a more expensive mix, or that the marginal fuel became much costlier.

Long-term pressures make every shock more expensive

Short-term shocks don't hit a neutral system. They hit grids already under stress from aging infrastructure, uneven transmission buildout, difficult interconnection processes, and policy choices that shift major costs into retail rates.

Consider the structural categories that intensify every external shock:

| Pressure | Why it matters for prices |

|---|---|

| Grid modernization | Utilities recover major capital spending through regulated rates, which can raise fixed and volumetric charges. |

| Resilience mandates | Wildfire mitigation, hardening, and reliability spending add costs even when fuel prices stabilize. |

| Load concentration | Large new customers can require rapid upgrades that regulated systems often spread widely. |

| Policy design | State rules on procurement, cost recovery, and tariffs determine who pays and when. |

Global shocks rarely create domestic bill pressure on their own. They become politically dangerous when they collide with a grid that already needs expensive upgrades.

The deeper strategic conclusion is that governments can't separate energy security from tariff design. Foreign crises may trigger the first move, but domestic institutions decide whether that move becomes a broad affordability problem. In that sense, the current energy cost increase is less a temporary spike than a stress test of the entire pricing architecture.

From Global Markets to Household Wallets

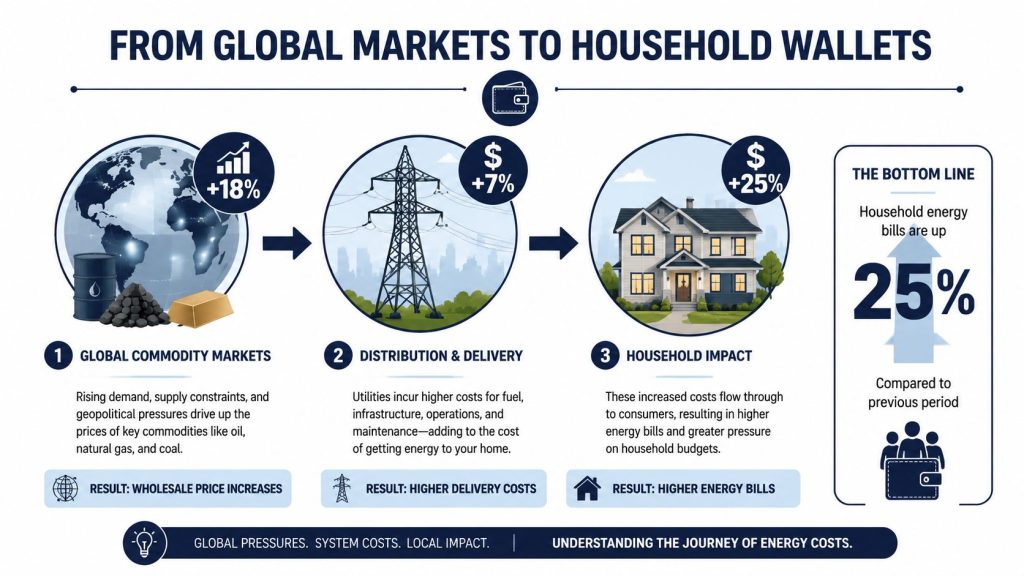

A rise in fuel costs doesn't arrive at the household as a headline. It arrives as a bill that's hard to parse. One line reflects energy consumed. Another covers delivery. Another may reflect prior utility spending approved through a regulatory process most customers never saw. By the time global turbulence reaches the customer, it no longer looks geopolitical. It looks personal.

How wholesale costs become retail pain

The transmission path is usually sequential. Fuel markets move first. Wholesale electricity prices respond. Utilities then seek to recover fuel, purchased power, infrastructure, and other approved system costs through retail rates. The public debate often compresses that process into “energy inflation,” but the policy mechanics are more specific.

A simple chain looks like this:

- Commodity markets tighten: Gas prices rise because of supply risk, sanctions, transport disruption, or changing trade flows.

- Power markets reprice: Gas often sets the marginal cost of electricity in many regions, so wholesale prices rise.

- Utilities absorb and file: Investor-owned utilities and other providers incorporate those costs into rate proceedings or adjustment mechanisms.

- Households pay unevenly: The final bill depends on housing quality, appliance efficiency, climate exposure, tariff structure, and income.

This distinction matters because policy tools differ at each stage. Strategic reserves, sanctions policy, and maritime security affect the first stage. Market design and rate oversight shape the later stages.

A short briefing video helps illustrate the consumer-facing dimension of this chain:

Why the burden is unequal

The distributional story is sharper than the average bill suggests. Recent coverage notes that average U.S. monthly electricity bills rose from about $121 in 2021 to roughly $156 in 2025, nearly a 29% increase, while low-income households face an average energy burden of about 8.6% of income versus 3.0% for other families, according to the NEADA Energy Affordability Project overview.

That means the same market shock produces different political realities. A moderate increase for a higher-income household can become a budgeting crisis for a family already spending a large share of income on essentials. NEADA also notes that older homes, inefficient appliances, and poor weatherization can waste 20 to 30% of consumed energy. That turns physical inefficiency into a social amplifier of price shocks.

The most important affordability metric isn't the average bill. It's the share of income required to keep the lights on.

For analysts, this changes the policy question. The issue isn't only why prices are up. The issue is which households have the least ability to absorb system costs they did not create. Once energy burden enters the picture, broad untargeted subsidies look less precise than reforms tied to efficiency, arrears relief, and rate design.

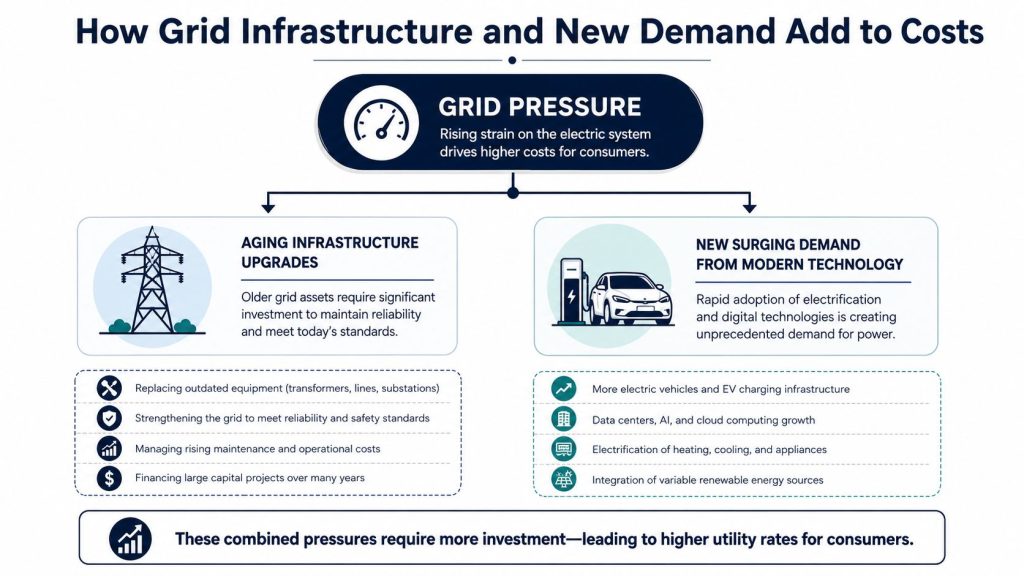

How Grid Infrastructure and New Demand Add to Costs

Fuel prices explain only part of the current energy cost increase. The less visible driver sits inside the grid itself. Utilities are being asked to connect a wave of new, power-intensive demand while also upgrading equipment, expanding substations, and reinforcing transmission systems that were not built for that pace of change.

Interconnection is now a price issue

The most striking number in this area is the scale of data-center demand. In 2025, U.S. utilities received requests for at least 700 GW of new data-center power connections, a figure that exceeds total U.S. electricity consumption in 2023, cited in the source as 477 GW-equivalent annual consumption, according to the EESI analysis of data-center electricity demand and rate pressure.

That figure should change how policymakers think about load growth. These aren't incremental additions. They are requests large enough to force system redesign. New substations, transformers, and transmission upgrades require capital. In regulated systems, that capital is commonly recovered through rates.

The same EESI analysis reports that in Virginia, electricity prices have increased by up to 267% over five years in data-center-heavy areas. The technical mechanism is simple even if the politics are not. When peak demand grows faster than firm generation and delivery capacity, utilities must accelerate upgrades and may rely on higher-cost market power in the meantime.

Rate design decides who pays

The key issue is not whether grids should be expanded. They should. The issue is who pays for expansion triggered by concentrated new load.

Here are the main policy fault lines:

- Socialized upgrade costs: Utilities often spread transmission and distribution investments across broad customer classes, which can make ordinary households subsidize infrastructure driven by large commercial entrants.

- Timing mismatch: Large customers seek rapid interconnection, but generation and wires infrastructure take time to build, creating a temporary cost squeeze.

- Peak-driven expense: It's not just total consumption. A customer that raises system peak can impose outsized costs on everyone else.

- Opaque tariffs: If tariff structures don't clearly assign incremental system costs to the customers causing them, cross-subsidies become politically difficult to defend.

A concise comparison helps:

| Question | Weak policy response | Stronger policy response |

|---|---|---|

| Who pays for upgrades tied to new load? | Spread widely across all customers | Assign more directly to incremental demand drivers |

| How are interconnection costs shown? | Buried in general rates | Disclosed transparently in tariff design |

| What happens during delays? | Existing customers absorb interim pressure | Temporary pricing signals reflect scarcity and timing |

If a grid connects high-value new industry but masks the cost allocation, the result isn't just higher rates. It's a legitimacy problem.

Geopolitics returns to the domestic arena. Governments want data infrastructure, strategic industries, and digital capacity for competitiveness. But if the electricity system finances that ambition through diffuse household bills, industrial policy can become electorally toxic.

Analyzing the Economic and Political Fallout

Household energy bills now carry foreign policy risk, industrial policy risk, and electoral risk at the same time. Once costs rise enough to be felt monthly, voters do not parse fuel markets, transmission upgrades, storm hardening, or utility accounting. They register that a basic service costs more and that public institutions approved it.

Utility regulation has become mass politics

That shift changes the function of rate cases. They are no longer confined to technical debates over prudent investment and allowed returns. They have become a public test of whether the state can protect affordability while still financing reliability, resilience, and new supply.

The political problem is sharper because the underlying drivers sit at very different levels of the system. A disruption tied to sanctions, shipping risk, or regional escalation can raise fuel and commodity costs. At the same time, domestic utilities are asking regulators to recover spending for grid modernization, wildfire mitigation, and generation additions. Add large new loads from data centers and advanced manufacturing, and the public sees one outcome: a larger bill. The distinction between external shock and local cost allocation disappears.

That feedback loop matters for foreign policy as much as for utility politics. Governments have more room to sustain sanctions or absorb instability abroad when households are not already under pressure from electricity, heating, and insurance costs. Debates at the United Nations over Iran-related pressure and diplomacy therefore connect directly to domestic affordability. If Gulf tensions raise input costs and those costs land in retail bills during an already contentious rate cycle, support for a harder external posture can weaken quickly.

Several consequences follow:

- Regulators face a credibility test: Even economically defensible approvals can trigger backlash if customers cannot see who caused which costs.

- Elected officials absorb indirect blame: Voters rarely separate commissions, utilities, legislatures, and federal policy into neat categories.

- Utilities face a trust constraint: A company may need real investment, but public consent erodes if every system need appears as a general rate increase.

- Foreign policy choices narrow: Energy-sensitive voters are less likely to tolerate prolonged external pressure campaigns when domestic bills are rising.

High power costs reshape investment decisions

The business effect is less visible but strategically important. Firms can manage short periods of volatility. What changes investment behavior is persistent uncertainty over future tariffs, connection timelines, and whether a jurisdiction will socialize the cost of expansion or assign it more directly to new demand.

That matters for regional development strategy. States want semiconductor plants, logistics hubs, and data centers because they promise tax revenue, jobs, and political prestige. But if rapid load growth forces near-term network upgrades that flow broadly into retail rates, the same projects can produce local opposition. Industrial policy then collides with utility politics at the meter level.

The resulting trade-offs are straightforward:

| Actor | Immediate effect | Strategic consequence |

|---|---|---|

| Households | Higher and less predictable monthly bills | More arrears, sharper voter anger, lower tolerance for policy trade-offs |

| Utilities | Heavier scrutiny of spending plans | Slower approvals and weaker public acceptance for future projects |

| Large power users | Uncertain tariffs and interconnection timing | Delayed siting decisions or relocation to jurisdictions with clearer cost rules |

| Governments | More pressure on inflation and affordability | Less room to balance sanctions, reindustrialization, and decarbonization goals |

High energy costs reduce more than purchasing power. They reduce governing capacity.

That is the deeper fallout. A system that passes global instability and domestic expansion costs into opaque retail bills does not just create economic stress. It weakens confidence in regulators, complicates industrial strategy, and makes foreign policy harder to sustain at home.

Navigating the New Energy Reality Policy Levers and Takeaways

Utility bills become politically dangerous when global shocks are socialized through domestic rate design without clear rules on who pays, why, and for how long. The policy problem is therefore narrower and more practical than headline debates suggest. Governments need mechanisms that absorb volatility, assign new system costs more precisely, and protect households that have the least room to adjust.

Affordability policy should start with targeting. Broad price suppression weakens price signals, obscures the source of cost increases, and often benefits higher-usage customers as much as vulnerable ones. Support is more defensible when it is tied to energy burden, arrears risk, medically necessary consumption, and housing conditions that make bills structurally harder to reduce.

Three implications follow.

- Direct support should go to high-burden households. Relief is most effective when it is linked to ability to pay rather than spread across all customers.

- Bill assistance should be paired with efficiency measures. Poor insulation, aging electric heating, and inefficient appliances turn temporary price pressure into chronic arrears.

- Bills should separate cost categories clearly. Customers and regulators need to see the difference between fuel costs, network upgrades, wildfire mitigation, resilience spending, and demand-driven expansion.

The harder question is cost allocation. Geopolitical stress can raise fuel and equipment costs. Sanctions, shipping disruption, and commodity volatility can then feed into utility procurement and capital plans. But the final bill impact depends on local regulatory choices: whether those costs are deferred, socialized across all customers, or assigned to the users and projects that drive them.

That point now matters beyond traditional utility planning. Data center growth, semiconductor manufacturing, and transport electrification are adding large, concentrated loads in specific regions. If regulators roll the grid upgrades required for those loads into general residential rates, industrial policy starts to look like a household tax. If they assign a larger share of interconnection and network expansion costs to new large users, states may preserve public support while still competing for investment.

Recent evidence from California illustrates the stakes. A CATF summary states that wildfire-related expenditures accounted for roughly two-thirds of 2019-2024 rate increases in the state, and that wildfire-related costs rose from 1.7% of retail rates in 2019 to 17% in 2024. The same summary reports that state renewable portfolio standards of 50% or higher were associated with about 5.1 cents/kWh higher electricity prices, while 100% RPS standards added 6.8 cents/kWh in the final model, according to the CATF review of rising U.S. electricity costs and policy solutions.

The policy conclusion is not that decarbonization, resilience, or reindustrialization should slow. It is that each objective needs a visible financing logic. Voters are more likely to tolerate expensive choices when governments identify the driver, the beneficiary, and the time horizon for recovery.

A workable policy package would include four elements:

- Visible recovery of resilience costs. Utilities should justify wildfire mitigation, grid hardening, and reliability spending in a format that lets regulators and customers distinguish protection from routine expansion.

- Clear marginal pricing for large new loads. Data centers and other major entrants should face tariff structures and interconnection terms that reflect the network costs they trigger.

- Integrated planning across generation, transmission, and demand. New load commitments without synchronized supply and wires investment increase the probability of repeated rate cases and reliability stress.

- Direct political accounting of trade-offs. Security policy, sanctions, decarbonization, and industrial strategy all carry system costs. Hiding those costs inside opaque retail bills weakens public consent.

The strategic takeaway is that energy policy now sits inside inflation management, industrial competitiveness, and foreign policy credibility. States that fail to connect macro shocks to retail rate mechanics will keep turning external crises into domestic political damage.

Vanitiro tracks exactly this kind of crossover story: how conflict, sanctions, shipping disruptions, and power politics move from foreign policy into domestic economics and everyday life. If you want concise, well-sourced analysis on the links between geopolitical risk and issues like energy cost increase, follow Vanitiro.