You may be looking at a life insurance policy you bought years ago and asking a hard question: does this contract still fit the life you have now? The policy may have built cash value, but the premiums feel less appealing, the features look dated, or your priorities have shifted from pure death-benefit protection toward retirement income or long-term care planning.

That's where 1035 exchange life insurance enters the picture. It isn't a loophole or a paperwork trick. It's a narrow tax rule that can let a policyholder move from one qualifying contract to another without immediately recognizing gains, but only if the exchange is structured correctly and only if the new policy is better for the policyholder after all costs, risks, and lost features are counted.

Most commentary stops at the tax benefit. That's not enough. The decision is whether tax deferral justifies giving up an older contract and taking on a new one. For many people, that's the difference between smart repositioning and an expensive mistake.

Table of Contents

- Why Your Old Life Insurance Policy May Not Be Your Last

- What Is a 1035 Exchange and How Does It Work

- The Rules of Engagement for a 1035 Exchange

- When a 1035 Exchange Makes Strategic Sense

- Executing the 1035 Exchange Transaction

- Balancing Tax Benefits Against Potential Trade-Offs

- Key Considerations Before You Make the Exchange

Why Your Old Life Insurance Policy May Not Be Your Last

A life insurance policy is usually purchased for a specific moment. A young family needs income protection. A business owner needs coverage tied to succession or liquidity. A higher earner wants permanent insurance with cash accumulation. Years later, the original reason may be weaker, but the contract remains.

That creates a familiar planning problem. The old policy may still hold meaningful cash value, yet keeping it no longer feels efficient. Surrendering it outright can raise tax concerns if gains have accumulated inside the contract. Holding it forever may preserve features you no longer need. Replacing it might solve one problem while creating three new ones.

A 1035 exchange exists for this kind of situation. It gives policyholders a way to replace a qualifying contract without immediate taxation on embedded gains, provided the exchange follows strict rules. Used well, it can help align old insurance assets with current objectives. Used casually, it can wipe out valuable policy history and expose the owner to fresh charges and restrictions.

Practical insight: The right question usually isn't “Can I exchange this policy?” It's “After taxes, charges, guarantees, and future goals, should I?”

That shift in framing matters. A policy with disappointing performance might still be worth keeping if it carries favorable guarantees or riders that would be expensive, unavailable, or medically difficult to replace. A policy that looks outdated on paper may still outperform a new contract once replacement friction is counted.

Policy analysis works best when it starts with purpose, not product. Before looking at forms or carriers, identify what problem the old policy is causing. Is it cost? Flexibility? Long-term care exposure? Estate planning no longer needed? That discipline matters in any serious publication focused on strategic trade-offs, including broader policy-oriented commentary such as the analysis collected in the Vanitiro blog archive.

What Is a 1035 Exchange and How Does It Work

A policyholder buys permanent life insurance at 35, builds cash value for decades, then reaches 60 and realizes the contract no longer fits the job. Premiums may be less efficient than newer designs. Riders may no longer match family needs. Surrendering the policy could solve the product problem while creating a tax bill. A 1035 exchange exists for that narrow but common tension.

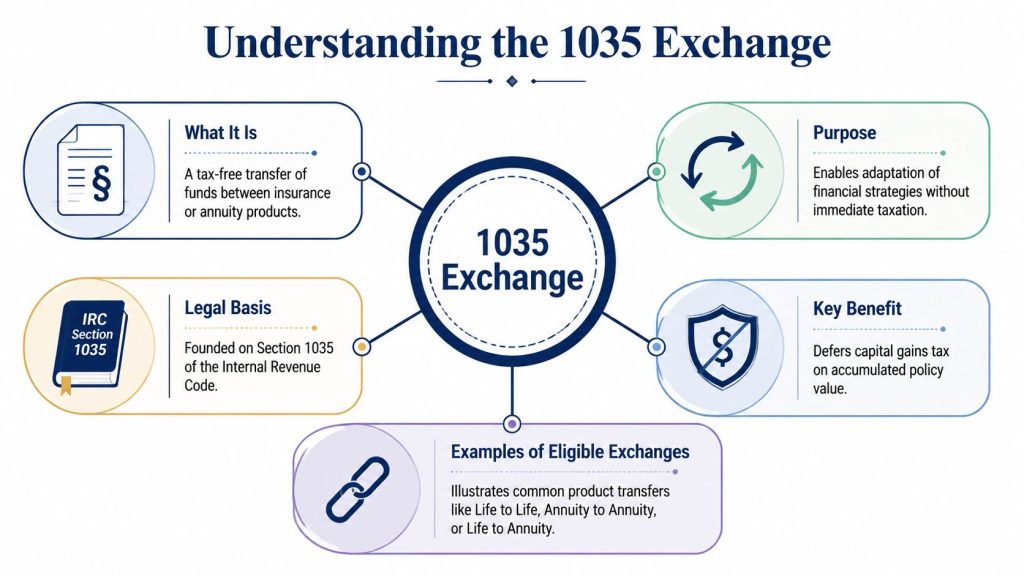

A 1035 exchange takes its name from Section 1035 of the Internal Revenue Code. It permits certain life insurance and annuity contracts to be exchanged without immediate taxation on gain inside the original contract, as explained in FINRA's discussion of insurance policy exchanges. The tax result matters because a surrender is generally a recognition event, while a qualifying exchange preserves tax deferral.

The practical effect is straightforward. The value moves from one eligible contract to another without first passing through the policyholder as a taxable cash-out. The accumulated gain is not forgiven. It carries over into the replacement contract, so the owner keeps the deferred tax position while changing products.

What the tax benefit actually protects

The benefit protects timing, not economics. If an older policy has cash value well above the owner's basis, surrendering it may trigger ordinary income on the gain. A 1035 exchange defers that recognition. For households trying to reposition insurance assets without creating current taxable income, that can preserve flexibility.

But tax deferral should not be mistaken for a free reset. The old contract's tax history follows the money into the new one. If the replacement policy later underperforms, imposes higher charges, or creates new access restrictions, the owner has still traded one set of economics for another. The exchange changes the wrapper and the future cost structure. It does not erase the consequences of a poor product choice.

Which exchanges are generally allowed

Section 1035 allows only certain directions of movement. A life insurance policy can generally be exchanged for another life insurance policy or for an annuity. An annuity generally cannot be exchanged for life insurance, as noted earlier from FINRA.

That one-way structure reflects the policy logic behind the rule. Congress allowed continuity across related insurance products, but not a tax-free conversion from an annuity back into life insurance. In decision terms, that means some exchanges preserve optionality and others permanently narrow it.

A useful way to evaluate a proposed exchange is to separate three distinct questions:

- Tax treatment: Will the transaction defer gain, or will it be treated as a taxable surrender?

- Product eligibility: Is the old contract being exchanged into a type that Section 1035 permits?

- Strategic fit: Does the new contract improve the owner's long-term position after fees, guarantees, underwriting, and liquidity limits are considered?

This is why a 1035 exchange is more than a form-processing exercise. It is a tax election embedded inside a product replacement decision, and the best choice is often the one that improves the total outcome, not merely the immediate tax result.

The Rules of Engagement for a 1035 Exchange

A policyholder who has built substantial cash value may assume the hard part is choosing a better contract. Under Section 1035, the harder part is often preserving the tax treatment while making that change. A replacement that looks sensible on financial grounds can still trigger current taxation if the exchange is executed in the wrong form.

Direct transfer is required

For Section 1035 treatment, the transaction generally must be carried out as a direct insurer-to-insurer transfer, as explained in Western & Southern's overview of 1035 exchanges. The old carrier transfers the value directly to the new carrier. The policyholder does not take control of the proceeds in between.

That formal step has a practical purpose. It separates an exchange from a surrender. If the owner receives the money first, even briefly, the IRS may view the old contract as cashed out and the new one as a separate purchase. In that case, any gain in the old policy can become taxable as ordinary income.

This is one reason a 1035 exchange should be evaluated as both a tax transaction and an implementation process. A better policy does not help much if the method of transfer turns a deferred gain into a current tax bill.

Continuity of parties limits how much can change

Qualification also depends on continuity. The owner and the insured or annuitant generally need to remain the same. As noted earlier, changing those identities can prevent the transaction from qualifying under Section 1035.

That rule often collides with real planning goals. A family may want to repurpose existing cash value to cover a different person, alter ownership for estate planning, or move the contract into a new structure. Those objectives may be reasonable, but they are not always compatible with tax-free exchange treatment. The trade-off is clear. The more a replacement changes the legal identity of the contract, the less likely it is to preserve the old policy's tax basis without recognition of gain.

Common mistakes that change the tax result

Several errors repeatedly turn an intended exchange into a taxable event or a nonqualifying replacement:

- Taking possession of the proceeds: If the owner receives the funds, the IRS may treat the old policy as surrendered.

- Changing the insured person: That can break the continuity Section 1035 generally requires.

- Liquidating and then buying separately: A sale followed by a new purchase is not the same as an exchange.

A simple comparison shows where the line usually falls:

| Action | Likely treatment |

|---|---|

| Old insurer transfers value directly to new insurer | Generally consistent with 1035 treatment |

| Owner receives a check, then buys a new policy | Can be treated as a taxable distribution |

| Same owner and insured continue on the new contract | Generally consistent with continuity |

| New insured replaces the old insured | Can jeopardize tax-free treatment |

The broader lesson is strategic, not just procedural. Section 1035 protects continuity of investment in insurance, not every sensible replacement decision. Someone who wants to change products, ownership, and insured lives at the same time may have to choose between tax deferral and greater planning flexibility. That is the core rule of engagement. The tax benefit is available, but only within a narrow set of transactional boundaries.

When a 1035 Exchange Makes Strategic Sense

A common real-world case looks like this: someone owns a permanent life insurance policy bought decades ago, has meaningful cash value, and no longer needs the same kind of death benefit. Surrendering the policy could trigger tax on gain. Keeping it may preserve tax deferral but leave money trapped in a contract that no longer fits the job. A 1035 exchange makes strategic sense when the tax cost of exiting is high, but the economic case for staying is weak.

That is a narrower standard than many sales discussions imply. The question is not whether a newer policy has attractive features. The question is whether changing contracts improves the owner's position after accounting for new charges, underwriting risk, surrender exposure, and any benefits that disappear once the old policy is gone.

An old permanent policy no longer fits the current objective

A policy purchased for income replacement often becomes misaligned later in life. Children become financially independent. Mortgages shrink or disappear. Estate liquidity, supplemental retirement planning, or long-term care funding may become more important than the original death benefit design.

In that setting, a 1035 exchange can serve as a capital reallocation tool inside the insurance system. It lets the owner carry tax basis and deferred gain into a different qualifying contract, which may be more useful than holding a legacy policy out of tax caution alone.

The trade-off is practical, not theoretical. Older contracts can contain favorable guarantees, established underwriting status, or riders that would be expensive or unavailable today. An exchange makes more sense when those legacy advantages are limited, and when the new contract solves a problem the old one handles poorly.

Long-term care planning can justify the change

The Pension Protection Act of 2006 expanded the planning value of Section 1035 by allowing certain tax-free exchanges into qualifying long-term care arrangements, including some hybrid products and, in some cases, tax-qualified long-term care insurance, as explained by the American Association for Long-Term Care Insurance.

That change widened the decision framework. For some older policyholders, the best use of accumulated cash value is no longer additional life insurance. It is help with a later-life risk that can disrupt retirement assets far more directly than an unneeded death benefit can protect them.

This does not make long-term care funding the automatic answer. It means Section 1035 can support a shift from legacy protection planning to care financing when the owner's balance sheet, family situation, and coverage priorities have changed.

The strategic value of a 1035 exchange often lies in changing the purpose of the dollars without accelerating tax.

Partial exchanges can be more disciplined than full replacement

A full policy replacement is not always the best solution. As noted earlier, industry guidance recognizes partial 1035 exchanges as a common way to reposition only part of a contract's value, especially in long-term care planning.

That matters because many insurance problems are specific, not total. An owner may want to preserve part of an existing policy for its guarantees or death benefit while shifting a portion of the value to address a newer need. In decision-making terms, that can be more efficient than replacing the entire contract because one feature no longer works well.

Partial repositioning also imposes analytical discipline. It forces a narrower question: how much of the existing policy still deserves to be kept?

Consolidation can help, but only if the economics improve

Some policyholders reach a point where multiple small legacy contracts create more administrative burden than planning value. Premium schedules differ. Riders vary. Monitoring performance becomes harder. A single replacement structure may be easier to manage and easier for family members to understand.

Even so, simplification is a secondary benefit, not a sufficient reason by itself. A less cluttered insurance portfolio can still be a worse financial result if the new policy introduces higher ongoing costs, weaker guarantees, or a longer path to break even.

A good 1035 exchange reduces mismatch. It does not just reduce paperwork.

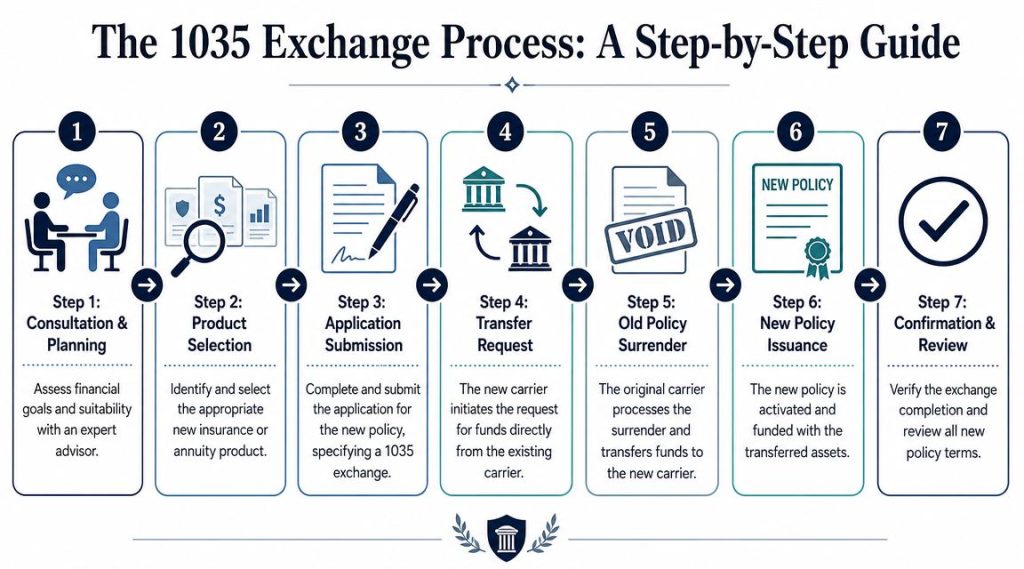

Executing the 1035 Exchange Transaction

A good exchange process feels procedural because it is. The legal rule is strict, and the operational workflow should reflect that. Most problems arise not at the level of theory but in forms, timing, underwriting, and coordination between insurers.

Early in the process, it helps to visualize the full sequence.

Start with a side-by-side contract review

Before anyone signs exchange paperwork, compare the current policy and the proposed policy on the issues that drive value. Look at surrender exposure, existing riders, death benefit structure, premium obligations, loan provisions, and how the policy fits the objective that now matters.

At this point, many replacement discussions become too sales-driven. The right baseline is not “Is the new policy attractive?” It is “Is the new policy better than keeping the old one after replacement costs and lost rights are counted?”

A focused review should answer questions like these:

- What problem is the existing policy failing to solve?

- Which current features would be lost permanently after surrender?

- Is the new policy dependent on fresh underwriting?

- What happens if the exchange starts but the new policy is delayed or issued on worse terms?

Decision rule: Never approve an exchange because the new product looks strong in isolation. Approve it only if it wins against the old contract in context.

Submit the new application correctly

The new insurer usually drives the transaction. The policyholder applies for the replacement policy and completes the carrier's 1035 exchange forms authorizing the transfer from the old insurer. This paperwork is not a minor administrative add-on. It is the mechanism that signals the transaction should be handled as an exchange rather than as a cash distribution.

Underwriting can complicate this stage. A policyholder may expect a straightforward replacement and discover that age, health status, or changed underwriting standards make the new policy more expensive or less favorable than expected. That risk should be resolved before the old contract is surrendered whenever possible.

A short video can help make the sequence more concrete.

The transfer stage is where precision matters

Once the new application is accepted and exchange instructions are in place, the new carrier requests funds directly from the old carrier. This is the critical “black box” period for many policyholders. They've signed documents, but they don't control the transfer themselves.

That loss of control is intentional. The law favors direct movement between carriers because direct movement preserves the exchange form. The policyholder should monitor status, but should not insert themselves into the payment chain.

Confirm the new contract, then re-check the economics

At the end of the process, the old policy is surrendered and the new contract is issued and funded with the transferred value. That doesn't mean the review is over. The policyholder should confirm that the issued policy matches the product and assumptions used to justify the exchange in the first place.

A post-issue checklist should include:

- Policy form accuracy: Confirm the issued policy is the intended product and rider package.

- Funding verification: Make sure transferred values posted correctly.

- Ownership review: Check that owner and insured information match the intended exchange structure.

- Retention file: Keep exchange forms, policy statements, and insurer correspondence together.

An exchange that is legally valid can still be strategically weak. Final confirmation is the last chance to catch that distinction.

Balancing Tax Benefits Against Potential Trade-Offs

A policyholder exchanges an older cash value policy, avoids immediate tax recognition, and feels relieved. Five years later, the new contract has higher ongoing charges, a fresh surrender schedule, and no longer includes an old rider that would have mattered in retirement planning. That outcome is possible because a 1035 exchange solves a tax problem, not every economic problem.

The main tax advantage is basis and gain carryover. The replacement policy generally takes the old policy's tax basis, so gain is deferred instead of recognized at the time of exchange, as explained in DA Davidson's discussion of basis carryover, MEC risk, and replacement costs. That treatment can also help preserve the existing tax position when cash value is repositioned, but it does not erase the policy's prior tax history or guarantee a better long-term result.

New costs can consume the tax advantage

Tax deferral has value only if the new contract improves the policyholder's net position after costs, guarantees, and expected use. New surrender charges, a restarted surrender period, different mortality assumptions, and higher policy expenses can shift value back to the insurer.

This is why exchange analysis should be comparative, not tax-centered. A recommendation is stronger when it measures the deferred tax against the cost of replacing the old contract, including charges that may not be obvious in a sales summary.

Legacy policy features can be more valuable than they look

Older contracts sometimes include benefits that are difficult or impossible to replace on current policy forms. The issue is not nostalgia. It is contract economics.

An older guarantee, rider design, or policy crediting structure may fit the insured's age, health status, or estate plan better than a newer product that looks cleaner on an illustration. Once the old policy is surrendered, those terms are usually gone permanently. That makes forgone features part of the exchange cost, even though they do not appear as a line-item tax charge.

A more disciplined comparison looks like this:

| Question | Why it matters |

|---|---|

| What tax is being deferred? | Shows the actual value of Section 1035 treatment |

| What new charges or restrictions begin? | Identifies costs that can offset the deferral benefit |

| Which contractual rights disappear? | Captures replacement risk that illustrations often understate |

| Does the new policy better serve the long-term objective? | Keeps the decision tied to planning goals, not just tax timing |

Carryover basis preserves complexity too

The basis carries forward. So do many of the planning consequences.

Future withdrawals, loans, and surrenders still need to be evaluated against the inherited basis and the new contract's structure. In practice, the exchange delays recognition rather than simplifying the tax picture. Readers interested in the broader policy logic behind that trade-off can see similar patterns in economic analysis of tax and financial regulation.

The practical conclusion is straightforward. A 1035 exchange is often best viewed as a reallocation decision under tax shelter, not as a free upgrade. The tax code may let a policyholder move without current recognition, but the market still charges for new guarantees, new risk assumptions, and new distribution costs.

Key Considerations Before You Make the Exchange

A sound exchange recommendation should survive skepticism. If an adviser or agent can't explain why the new policy is better than the old one using contract-specific evidence, that's a warning sign.

Ask for the existing policy's in-force illustration and a full projection for the proposed policy. Review them side by side. Don't settle for broad claims about “better performance,” “modern features,” or “improved efficiency” unless those advantages are tied to identifiable policy terms.

A useful set of questions includes:

- What exact problem does the exchange solve? If the answer is vague, the recommendation is weak.

- What do I lose by giving up the current policy? That includes riders, guarantees, and policy age.

- What happens if underwriting changes the offer? The strategy should still make sense under less favorable assumptions.

- How is the adviser compensated? Incentives don't automatically invalidate advice, but they should be visible.

- What is the downside if I do nothing? The old policy should be evaluated as a live option, not as dead weight.

The best exchange recommendations are comparative, documented, and patient. The worst ones are urgent.

Finally, remember that the legal success of an exchange and the financial wisdom of an exchange are different things. A transaction can satisfy Section 1035 and still leave the policyholder worse off. The burden is on the recommendation to prove more than tax compliance.

If you want careful, context-driven reporting on policy, economics, and the strategic consequences of technical rules, you can follow ongoing coverage through the Vanitiro newsletter.

Vanitiro publishes clear, sourced analysis for readers who care about how policy choices shape real-world outcomes. If you value reporting that connects technical rules, strategic incentives, and broader public consequences, explore Vanitiro.