The iran central bank is often described as a failed monetary authority. That's true, but it misses the larger point. The more useful frame is that the Central Bank of Iran is one of the regime's core instruments of state power: it manages inflation badly, but it also helps the state absorb sanctions pressure, re-route financial flows, and preserve strategic room for action abroad.

That matters because the bank's technical decisions don't stay technical for long. They shape how Iran finances itself under pressure, how it manages access to foreign exchange, how it watches domestic money flows, and how regional risk gets priced into shipping and energy markets. If you want to understand why a currency crisis in Tehran can feed into a Strait of Hormuz premium or become part of a U.S. election-year sanctions debate, the CBI is one of the first institutions to examine.

Table of Contents

- The Central Bank as a Geopolitical Battleground

- Institutional Structure and Political Control

- Waging a Losing War on Inflation

- Foreign Reserves and Shadow Financial Networks

- The Digital Rial A Tool for Control

- Economic and Geopolitical Ripple Effects

- What Analysts Should Watch in 2026

The Central Bank as a Geopolitical Battleground

The Central Bank of Iran is not just a monetary institution. It is one of Tehran's main instruments for absorbing sanctions pressure, rationing hard currency, and keeping the state functional under economic siege.

Established in 1960 under the Monetary and Banking Act, the bank never developed into an independent inflation-fighting authority in the way many central banks did. Its role evolved inside a political system where exchange-rate management, fiscal accommodation, and sanctions resilience often mattered more than monetary discipline. That distinction shapes how the institution should be read. Analysts who treat the CBI as a technocratic policy actor miss its real function.

Its strategic importance rose as sanctions tightened and Iran lost normal access to dollar clearing, correspondent banking, and parts of the global payments system. Under those conditions, the CBI became a choke point. It allocates scarce foreign exchange, channels pressure away from politically sensitive sectors, and helps the state decide who gets liquidity and who absorbs the shock.

This matters beyond inflation.

A central bank that controls access to foreign currency also influences Iran's room for maneuver in regional crises. If oil revenues are disrupted, if shipping risks rise around the Strait of Hormuz, or if sanctions enforcement suddenly hardens, the CBI is one of the first institutions forced to convert geopolitical stress into domestic economic triage. Its decisions then feed back into energy markets, because traders price not only barrels and tankers but also Iran's capacity to settle trade, defend imports, and keep export flows moving through informal channels.

That is why the CBI belongs in security analysis as much as in economic analysis. It sits at the intersection of sanctions design, regime durability, and escalation risk. Financial restrictions debated in diplomatic forums can alter the bank's operating room, and that wider context is visible in reporting on United Nations pressure on Iran.

The broader implication is easy to miss. Weak central banking in Iran is not only a symptom of economic mismanagement. It is also part of a wartime-style state architecture, one built to survive isolation, shift costs onto households and firms, and preserve strategic freedom even as monetary credibility erodes.

Institutional Structure and Political Control

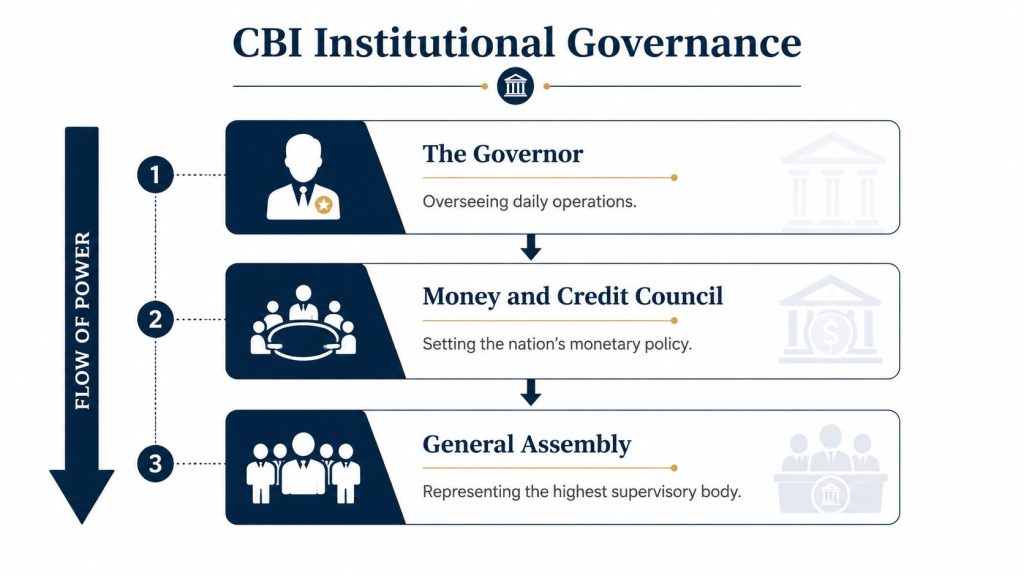

The Central Bank of Iran sits inside the state's command chain. That fact matters more than its formal charter, because the bank is expected to preserve regime resilience under sanctions as much as it is expected to manage money.

Formal hierarchy and real hierarchy

The institutional design appears familiar on paper. In practice, authority flows from the political system into the bank, not from the bank outward into policy.

| Body | Formal role | Strategic reality |

|---|---|---|

| Governor | Oversees daily operations | Administers policy within political boundaries set elsewhere |

| Money and Credit Council | Sets monetary policy direction | Translates state priorities into financial decisions |

| General Assembly | Highest supervisory layer | Extends government oversight rather than independent scrutiny |

This arrangement shapes how analysts should read CBI behavior. A rate decision, a currency intervention, or a change in bank credit conditions can signal political priorities as clearly as economic ones.

Why independence never took hold

Central bank independence limits fiscal dominance. Iran's system was built for the opposite problem. The leadership needs a financial institution that can absorb sanctions pressure, direct credit to protected constituencies, and keep priority imports and state-linked networks functioning during external shocks.

That requirement narrows the bank's room to resist government demands. Monetary policy becomes subordinate to regime preservation, especially when sanctions tighten, oil revenue becomes less predictable, or external tensions raise the risk of trade disruption.

The operational implications are straightforward:

- Interest rates reflect political tolerance for pain, not only inflation risks.

- Credit allocation supports sectors and institutions tied to regime stability.

- Exchange-rate management helps ration foreign currency under pressure.

- Liquidity creation can backstop state spending even when it weakens monetary credibility.

For analysts, the main question is simple. Which political objective is the CBI protecting with each technical move?

The strategic consequence

This governance model makes the CBI more than a weak central bank. It makes the bank a state power instrument. That distinction helps explain why sanctions policy often targets financial channels so aggressively. Restricting the CBI does not only constrain inflation management or balance-sheet flexibility. It narrows Tehran's ability to settle trade, shield favored actors, and convert hard-currency earnings into strategic endurance.

That has implications beyond Iran's domestic economy. In a Strait of Hormuz crisis, for example, the bank would be part of the state's first response to shipping risk, payment disruption, and import stress. In U.S. political debate, the same institution can become shorthand for whether sanctions are biting or leaking. The CBI therefore sits inside election narratives, oil risk pricing, and regional escalation calculations at the same time.

Technocrats still matter. Their discretion is real at the margin. But the hierarchy above them defines the mission, and that mission is political before it is monetary.

Waging a Losing War on Inflation

Iran's inflation problem reflects a state financing model under sanctions, not a temporary policy miss. The Central Bank of Iran is expected to contain prices while also supplying liquidity to a system under fiscal, banking, and external pressure.

As noted earlier, the long record is poor. Iran has lived with persistently high inflation and repeated liquidity surges for decades. That matters because it shows a pattern of political subordination, not an isolated failure by central bank technocrats.

Why conventional tools fail

A normal central bank can tighten credit, raise funding costs, and accept slower growth to restore credibility. The CBI operates inside a narrower corridor. It faces demands to support state spending, stabilize banks, and manage exchange-market stress at the same time.

Sanctions make that tradeoff harsher. They restrict access to hard currency, weaken fiscal flexibility, and increase the premium on any channel that can keep imports paid and politically sensitive sectors funded. Under those conditions, anti-inflation policy competes directly with regime preservation.

The sequence is familiar:

- Fiscal pressure rises.

- Banks absorb part of the strain.

- The CBI adds liquidity or eases constraints.

- Prices and exchange-rate expectations worsen.

- Households shift into dollars, gold, goods, or property.

- The state responds with more controls, not full monetary restraint.

This cycle helps explain why inflation in Iran is strategically important. It is one of the clearest indicators of whether the regime is financing resilience by eroding the currency.

Inflation is a political signal

The main constraint is fiscal dominance. The bank can issue plans, adjust administered rates, and tighten selectively. It cannot impose lasting discipline if the state still needs monetary expansion to cover deficits, support weak banks, and cushion sanctions shocks.

That turns inflation into a measure of state stress. Rising prices signal that Tehran is transferring the cost of sanctions and external isolation onto domestic balance sheets. Households pay through weaker wages, lost savings, and exchange-rate insecurity. Businesses pay through shorter planning horizons and stronger incentives to speculate rather than invest.

The geopolitical consequence is often underestimated. A government dealing with chronic inflation has less room to absorb external shocks peacefully. If tensions in the Strait of Hormuz disrupt shipping or raise import costs, the monetary effect reaches Iran quickly through prices, currency demand, and subsidy pressure. The CBI then becomes part of crisis management, not because it controls escalation, but because it must keep payments moving and panic contained.

That also helps explain why the bank appears in U.S. political narratives. Inflation and currency weakness offer a visible test of whether sanctions are constraining Tehran or leaving room for adaptation. For analysts, the point is straightforward. Persistent inflation is not only an economic failure. It is evidence that the CBI is being used to convert financial isolation into temporary political endurance, at growing domestic cost.

Foreign Reserves and Shadow Financial Networks

The Central Bank of Iran's reserve position matters less as a balance-sheet statistic than as a measure of coercive capacity. Once reserves are frozen or trapped abroad, the CBI stops acting like a conventional lender of last resort and starts acting like a sanctions survival office.

Iran still has external assets. The constraint is access, timing, and convertibility, as noted earlier. That distinction matters. A country can appear solvent on paper while remaining cash-constrained in the transactions that fund imports, stabilize the currency market, and support regional clients. For Tehran, blocked reserves do not just weaken macroeconomic management. They force the state to build parallel channels for trade settlement, oil receipts, and cross-border transfers outside normal banking supervision.

How reserve pressure changes the bank's function

Reserve restrictions push the CBI into a different operating model. It must help the state preserve hard-currency inflows, obscure beneficial ownership, and reduce exposure to Western compliance filters. That means using front companies, exchange houses, informal transfer networks, and banks in jurisdictions willing to tolerate higher sanctions risk.

Dubai, Turkey, and parts of Asia matter for a simple reason. They offer commercial density, logistics links, and financial intermediaries that can reroute payments even when formal correspondent banking tightens. These hubs do not solve Iran's structural weaknesses. They buy time, reduce friction, and keep selected state priorities funded.

The strategic point is often missed. Reserve denial does not only drain resources. It changes which institutions matter. Under sanctions, the CBI becomes a coordinator of workaround finance across ministries, energy traders, state firms, and external partners.

A dispersed sanctions-evasion architecture

The more important shift is organizational, not technical. Reported movement toward offshore structures and alternate financial messaging systems suggests Iran is spreading risk across a wider network rather than relying on a few vulnerable channels. According to analysis of the CBI role in bypassing sanctions, U.S. Treasury actions in early 2026 highlighted networks that moved restricted oil revenue to regional allies and linked covert shipping activity to measurable energy-market effects.

That has two implications.

First, sanctions enforcement now targets a distributed system. Disrupting one bank, shipper, or intermediary no longer guarantees meaningful financial isolation if settlement can shift laterally through adjacent nodes.

Second, the line between monetary administration and regional power projection has narrowed. If oil proceeds routed through covert channels support allied militias or sanctioned partners, then CBI-linked financial operations are part of Iran's deterrence posture. They help sustain influence from the Levant to the Gulf while reducing the visible fiscal burden on the formal state budget.

Why this matters beyond Iran

This is not an internal Iranian finance story. Workarounds that preserve export revenue can soften the intended effect of sanctions, prolong Tehran's regional reach, and complicate U.S. claims about economic pressure during election cycles. They also matter for energy markets. If shadow shipping and off-book settlement keep barrels moving through periods of Gulf tension, traders must judge not only physical disruption risk in the Strait of Hormuz but also how much hidden export capacity Iran can still monetize.

Analysts should therefore watch the plumbing, not just the headline reserve figure. Changes in payment routing, shipping cover, settlement currencies, and intermediary jurisdictions often reveal more than official reserve estimates. Those signals show whether the CBI is losing room to maneuver or refining its role as an instrument of state resilience under sanctions.

The Digital Rial A Tool for Control

Many governments market central bank digital currencies as modernization. Iran's Digital Rial, or Ramzrial, is better understood as a control system that also happens to be a payment architecture.

The verified data describes it as a centrally controlled CBDC designed for total transaction traceability. It aims to counter an estimated $15B in oil revenues evaded annually through hawala networks, and to expand state surveillance through mandatory KYC for wallets holding more than 1 million IRR and real-time monitoring of transfers (analysis of Iran's Digital Rial and traceability design).

Not a decentralization story

The common mistake is assuming digital money makes finance more open. In Iran's case, the design points the other way.

The system is permissioned. Control is centralized. Traceability is a feature, not a side effect. The state gets a stronger map of who pays whom, when, and through which channels. That's useful for anti-money-laundering claims, but it's also useful for domestic coercion.

A concise comparison helps:

| Common CBDC assumption | Digital Rial reality |

|---|---|

| Modernization of payments | Expansion of centralized oversight |

| Convenience for users | Visibility for the state |

| Financial inclusion narrative | Surveillance and anti-evasion logic |

| Alternative to informal transfers | Tool to suppress informal transfers |

Why the bank wants it

The CBI has strong reasons to build this system.

- Capital flight pressure: More traceability can make it harder to move money.

- Hawala leakage: If informal channels are draining oil revenue, the bank wants better visibility.

- Tax enforcement: A digitized transaction record improves the state’s ability to see activity it previously struggled to observe.

- Sanctions adaptation: A domestic digital rail may strengthen internal control even if it doesn’t create a reliable external sanctions workaround.

A fully traceable CBDC can reduce one form of evasion while creating a richer intelligence target for foreign sanctions monitors.

The strategic paradox

The Digital Rial may strengthen the regime domestically while increasing its exposure externally. A tightly monitored ledger helps Tehran discipline internal flows, but it also creates a more legible system for anyone trying to understand state-linked transaction patterns.

That makes Ramzrial a double-edged project. It can narrow domestic financial opacity, yet it may not deliver the international freedom of movement that sanctions relief would provide. In other words, it’s less a path around sanctions than a tool for governing scarcity inside sanctions.

Economic and Geopolitical Ripple Effects

The CBI’s policy failures and sanctions workarounds don’t stop at Iran’s borders. They feed regional instability through financing channels, shipping risk, and the pricing of uncertainty.

The verified data on early 2026 Treasury action is especially important because it ties financial adaptation to strategic effects outside banking. It highlights Iran’s use of decentralized offshore banking to route $2-3 billion annually in restricted oil revenues to allies and notes that this covert activity can inflate global energy prices by 5-10% through untracked Strait of Hormuz shipments (reporting and analysis on energy market impacts).

Why energy traders should care

For markets, the central issue isn’t whether the CBI can restore macroeconomic normality. It’s whether the bank can keep enough money moving to sustain behavior that raises transport and supply risk.

That’s the connection many observers miss. A central bank decision about liquidity, reserves access, or informal payment channels can become a shipping insurance issue, a crude pricing issue, or a political issue in Washington.

Three ripple effects matter most:

- Regional proxy finance: If funds reach allied networks, security risk persists beyond Iran’s domestic economy.

- Hormuz risk premium: Financial opacity around shipments can widen uncertainty in a chokepoint that markets already treat as highly sensitive.

- Election narrative spillover: Energy price volatility can reshape sanctions debates in the United States, especially when inflation remains politically salient.

Domestic fragility and external leverage

The regime’s financial weakness doesn’t automatically reduce its geopolitical relevance. Sometimes it increases the incentive to generate influence abroad.

That’s why the iran central bank should be read not only as a distressed institution but also as a force multiplier. Under pressure, it helps convert financial scarcity into strategic improvisation. The result is a policy environment where seemingly narrow monetary decisions can feed directly into regional confrontation and global market anxiety.

What Analysts Should Watch in 2026

The right way to watch the iran central bank in 2026 isn’t to focus on one headline indicator. Analysts need a small dashboard that connects monetary stress, control mechanisms, and external operations.

Five indicators that matter

-

Leadership changes at the CBI

A leadership reshuffle can signal more than administrative turnover. It may indicate a harder political line, a failed stabilization effort, or a push to align the bank more closely with sanctions-evasion priorities. -

The pace and scope of the Digital Rial rollout

Watch whether the system stays limited or becomes more embedded in everyday transactions. Faster integration would suggest the regime is prioritizing visibility and internal control over financial flows. -

Signals around access to foreign exchange

Don’t just look for official claims. Watch for indirect evidence that pressure is easing or tightening, including shifts in enforcement narratives, changes in routing behavior, or more aggressive efforts to build alternative channels. -

Evidence of deeper offshore financial adaptation

The most consequential developments may not appear first in central bank statements. They may appear in sanctions actions, shipping investigations, or disclosures about new messaging and settlement pathways. -

The relationship between domestic monetary strain and external escalation When internal financial stress rises, the regime may have greater incentive to seek advantages abroad. Analysts should read financial and security indicators together, not separately.

Bottom line: A central bank under sanctions doesn’t behave like a normal monetary institution. It becomes a pressure gauge for the state itself.

How to interpret the signals

A useful rule is to ask what each indicator says about regime confidence. A cautious digital rollout, opaque reserve management, or abrupt personnel shifts may point to fragility. More assertive financial experimentation may point to adaptation, but also to rising enforcement risk.

The CBI also belongs in wider threat monitoring. Financial control, sanctions evasion, and coercive regional behavior often move in parallel. Readers following that broader security picture should keep an eye on ongoing analysis of the Iran nuclear threat and regional escalation risks.

The main conclusion is straightforward. The CBI isn’t just failing to stabilize prices. It is helping the Iranian state decide how to survive pressure, where to absorb pain, and how to convert financial constraint into strategic action.

Vanitiro tracks those linkages in real time, from sanctions enforcement and Iranian financial adaptation to Strait of Hormuz tensions and the energy consequences that reach global markets. If you need concise, source-driven geopolitical coverage that connects monetary signals to security outcomes, follow Vanitiro.